Journal Entry Sequences for Stock Dividends Format, Example

To illustrate, assume that Ironside Corporation declared a property dividend on 1 December to be distributed on 4 January. The maximum amount of dividends that can be issued in any one year is the total amount of retained earnings. If there is a deficit (negative balance) in retained earnings, any dividend would represent a return of invested capital. Suppose a corporation currently has 100,000 common shares outstanding with a par value of $10.

Stock Dividend

Sometimes companies choose to pay dividends in the form of additional common stock to investors. This helps them when they need to conserve cash, and these stock dividends have no effect on the company’s assets or liabilities. The common stock dividend simply makes an entry to move the firm’s equity from its retained earnings to paid-in capital.

Samsung Boasts a 50-to-1 Stock Split

Similar to the stock dividends, some companies may directly debit the retained earnings on the date of dividend declaration without the need to have the cash dividends account. This is usually the case which they do not want to bother keeping the general ledger of the current year dividends. When a dividend is later paid to shareholders, debit the Dividends Payable account and credit the Cash account, thereby reducing both cash and the offsetting liability. A stock dividend is a type of dividend distribution in which additional shares are distributed to shareholders, usually at no cost. These new shares are then traded on the same exchange at current market prices. Dividend payments also influence key financial ratios, such as the dividend payout ratio and the return on equity (ROE).

Dividends Declared Journal Entry

Clearly, a stock dividend conserves cash and thus allows the firm to use its cash for growth and expansion. Therefore the cost per share to the investor is reduced to $50 per share ($60,000 + 1,200 shares), from the original $60 per share. Subsequently, South Gulf issues a 20% stock dividend, and so the investor 10 essential tax questions for homeowners will receive an additional 200 shares (1,000 x .20). Since accountants at Your Co. have already created the liability (Dividends Payable) and have not yet paid the cash dividend, no accounting financial statement is changed. A stock dividend is a distribution of shares of a company’s stock to its shareholders.

Large stock dividend

As soon as the dividend has been declared, the liability needs to be recorded in the books of account as a dividend payable. Assuming there is no preferred stock issued, a business does not have to pay a dividend, the decision is up to the board of directors, who will decide based on the requirements of the business. Dividend payments are a critical component of the financial strategies for many companies, representing a tangible return on investment for shareholders. The process of recording these transactions is not merely a clerical task but an essential element of corporate accounting that ensures accuracy in financial reporting and compliance with regulatory standards. Dividend record date is the date that the company determines the ownership of stock with the shareholders’ record.

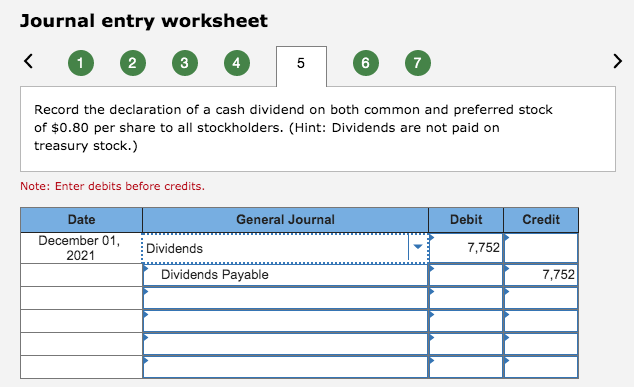

This entry is made at the time the dividend is declared by the company’s board of directors. The amount credited to the Dividends Payable account represents the company’s obligation to pay the dividend to shareholders. The debit to Retained Earnings represents a reduction in the company’s equity, as the company is distributing a portion of its profits to shareholders. When a company decides to distribute dividends, the accounting process begins with the declaration of the dividend by the board of directors. This declaration creates a liability for the company, as it now owes the declared amount to its shareholders. The initial journal entry to record this liability involves debiting the Retained Earnings account and crediting the Dividends Payable account.

Again, in order to pay a cash dividend, a firm must have the necessary cash available, and the amount of cash on hand is not directly related to retained earnings. This journal entry is to eliminate the dividend liabilities that the company has recorded on December 20, 2019, which is the declaration date of the dividend. While a few companies may use a temporary account, Dividends Declared, rather than Retained Earnings, most companies debit Retained Earnings directly. The most important thing to note by comparing the stockholders’ equity section in both balance sheets is that the total is $3 million In both cases. The only difference is the total of the various accounts within stockholders’ equity.

Deciding when to start paying dividends, how much to pay, and how frequently to pay them can be difficult. These can be key signals in the maturity of your business and optimism of the business owners or directors. Debiting the account will act as a decrease because the money that is being paid out would otherwise have been held as retained earnings. And not all businesses are strong enough to issue dividends year-in and year-out.

This does not require any journal entry, but many investors, especially short-term hold or day-trading investors, want to know this date so that they can buy the stock, receive the dividend and then sell the shares. The presentation of dividends in financial statements under IFRS also requires careful consideration. Dividends are typically disclosed in the statement of changes in equity, where they are shown as a deduction from retained earnings. Additionally, companies must provide detailed disclosures about their dividend policies, the amount of dividends declared and paid, and any restrictions on the payment of dividends. These disclosures help investors and analysts understand the company’s approach to profit distribution and assess its financial health and sustainability.

However, not all dividends qualify for this lower rate, and investors must meet specific holding period requirements to benefit from the reduced tax rate. The mechanics of dividend distribution involve several steps, each requiring meticulous attention to detail to reflect the company’s financial position accurately. From the moment dividends are declared to the point where they impact a company’s balance sheet, every entry must be carefully documented. With this journal entry, the statement of retained earnings for the 2019 accounting period will show a $250,000 reduction to retained earnings.

- For example, in Canada, the dividend tax credit allows individuals to reduce their tax liability on dividends received from Canadian corporations.

- Companies issue stock dividends when they want to bring down the market price of their common stock.

- The company basically capitalizes some of its retained earnings, moving it over to paid-in capital.

- Once the previously declared cash dividends are distributed, the following entries are made on the date of payment.

On the dividend payment date, the cash is paid out to shareholders to settle the liability to them, and the dividends payable account balance returns to zero. In some jurisdictions, tax credits or deductions are available to mitigate the impact of double taxation. For example, in Canada, the dividend tax credit allows individuals to reduce their tax liability on dividends received from Canadian corporations. This credit is designed to account for the corporate taxes already paid on the distributed profits, thereby reducing the overall tax burden on shareholders. Such mechanisms can significantly influence investor behavior and the attractiveness of dividend-paying stocks.