Step Cost Definition, Example, Formula, Functions, Applications

Step cost behaviors have significant implications for financial planning, budgeting, and decision-making. They require managers to be mindful of the activity levels at which cost changes occur, as these thresholds can impact pricing, profitability analysis, and capacity planning. Semi-variable Costs Semi-variable costs are costs that have both a variable and fixed component. Commercial leases often have a fixed rent per month plus an additional rent based on the amount of production or sales.

Examples

For example, rent is $5,000 plus five cents for each pencil that is made. The base rent of $5,000 is a fixed cost and the five cents per pencil is a variable cost. These changes in variable costs per unit could be caused by circumstances beyond their control, such as a shortage of raw materials or an increase in shipping costs due to high gas prices. In any case, average variable cost can be useful for managers to get a big picture look at their variable costs per unit. A step cost remains constant at a certain fixedamount over a range of output (or sales). A mixed cost contains a fixed portion of costincurred even when the facility is idle, and a variable portionthat increases directly with volume.

Financial and Managerial Accounting

If it’s just a small increase in volume, management may try to squeeze out extra productivity from existing operations, instead of incurring stepped-up costs. Unavoidable fixed costs are costs you have to incur if you want to stay in business. For example, the administrative costs of running a processing facility are an unavoidable fixed cost. Interest on term debt on the facility is also an unavoidable fixed cost.

Fixed Costs

For example, many auto mechanics are now paid a flat weekly or monthly salary. Why is it so important for Bert to know which costs are product costs and which are period costs? Bert may have little control over his product costs, but he maintains a great deal of control over many of his period costs. For this reason, it is important that Bert be able to identify his period costs and then determine which of them are fixed and which are variable. Remember that fixed costs are fixed over the relevant range, but variable costs change with the level of activity. If Bert wants to control his costs to make his bike business more profitable, he must be able to differentiate between the costs he can and cannot control.

Additional Resources

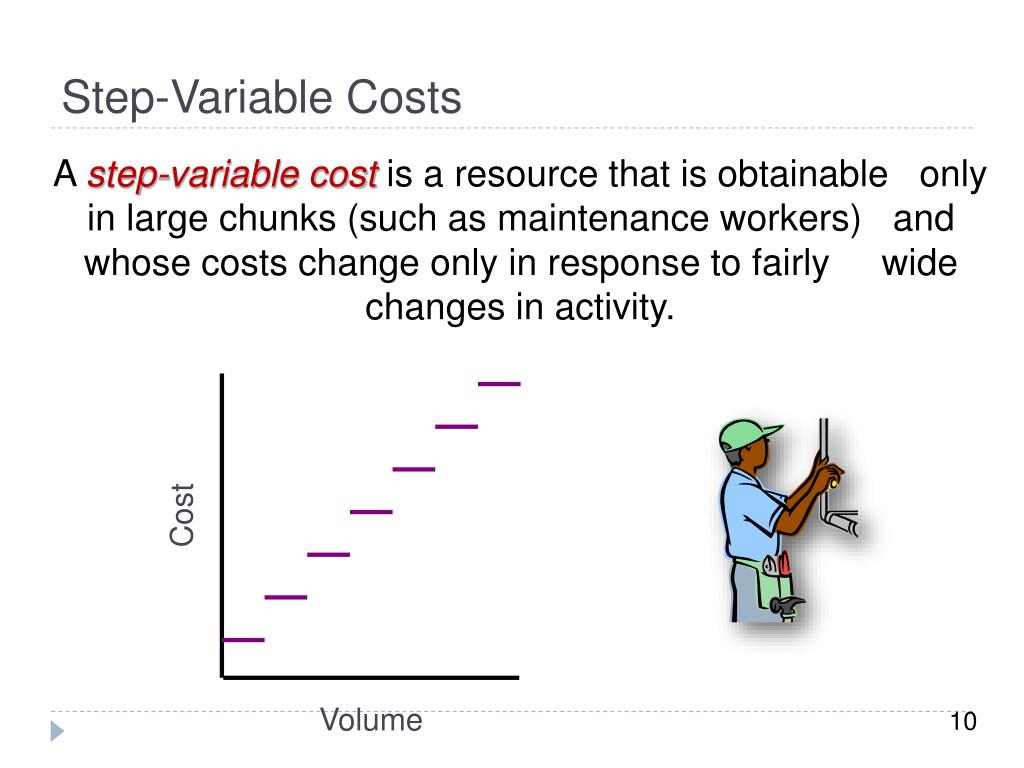

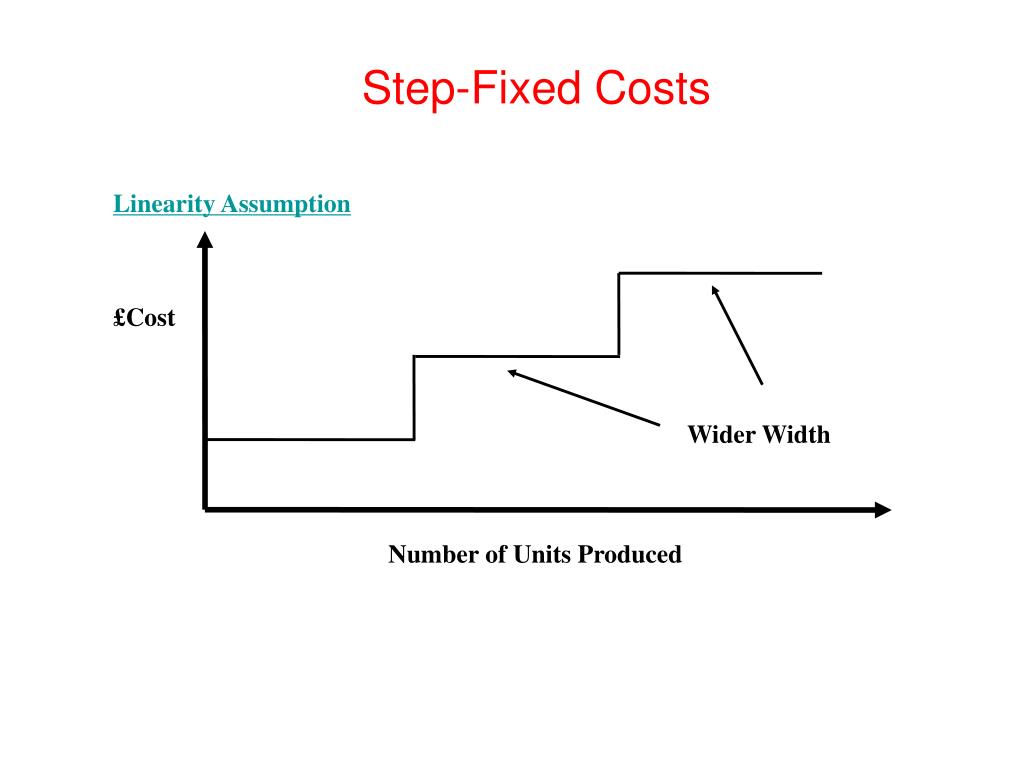

In other words, these costs do not change steadily with changes in activity level, but rather at discrete points over time. Variable cost is one key categorization of total costs incurred in a business unit. Every cost that explicitly changes with a change in the level of output or another business activity qualifies to be a variable cost. what is a triple net nnn lease and whats included in it Within variable costs as well, there are different cost categorizations based on their relationship with level of output. A stepped cost is also referred to as a step cost, a step-variable cost, or a step-fixed cost. The difference between a step-variable cost and a step-fixed cost has to do with the width of the range of activity.

Spring Break Trip Planning

He currently researches and teaches economic sociology and the social studies of finance at the Hebrew University in Jerusalem. In March 2023, they took significant steps towards carbon capture and storage (CCS). Chevron, the oil refinery company with a significant market share that sells various refined products such as gasoline, diesel, marine, and aviation fuels is headquartered in California.

- For this reason, it is important that Bert be able to identify his period costs and then determine which of them are fixed and which are variable.

- The labor cost to produce 401 units stepped up from $6,500 to $13,000.

- A cost that changes with the level of activity but is not linear is classified as a stepped cost.

As the company increases its volume ofactivity, it runs more machines and runs them longer. An example of step costs is a company that produces a certain product, deploying the machinery, production staff and workplace to produce a certain number of it per year (e.g., 20,000). If an order arrives requesting it to produce 30,000 per year for a period of three years. The company will start to incur step costs to account for the new production level. To that end, it requires to deploy additional machinery, personnel and plant as an additional cost per year.

Step cost refers to an expense that changes abruptly at certain activity levels or thresholds. Instead of gradually increasing with activity, the cost remains constant within a range but “steps up” to a higher level once a specific point is reached. This concept is crucial for budgeting, pricing, and decision-making, as it highlights the impact of reaching certain production or activity levels on overall costs. A step cost is a cost that does not change steadily with changes in activity volume, but rather at discrete points.

Table 6.6 illustrates the types of fixed costs for merchandising, service, and manufacturing organizations. Managers usually separate mixed costs into theirfixed and variable components for decision-making purposes. Theyinclude the fixed portion of mixed costs with other fixed costs,while assuming the variable part changes with volume. We will lookat ways to separate fixed and variable components of a mixed costlater in the chapter.

The moment you need a fourth account, your costs jump to $40 per month with the next level plan. The salary of a shop floor supervisor in a production department overseeing 1,500-2,000 units produced daily is an example of this concept. Understanding step costing is extremely important when a company is about to reach a new and higher activity level, where it will be required to traverse a large step cost. In some cases, the step cost may eliminate profits that management had been expecting with increased volume. By identifying the thresholds at which step cost behavior occurs, businesses can anticipate changes in their cost structure and adjust their strategies accordingly.

If the total cost increases with small increases in activity, it may be referred to as a step-variable cost. If the total cost will change only with large increases in the quantity of activity, the term step-fixed cost is more likely to be used. The function of a step cost is to represent the sudden and discrete changes in expenses that occur at specific levels of activity or production. Step costs play a crucial role in cost analysis, financial planning, and decision-making for businesses and organizations. (1) Pay the quality inspector overtime in order to have the additional units inspected.